Key Takeaway

South Korea's anticipated MSCI Developed Market upgrade is poised to reallocate trillions, creating a significant liquidity injection opportunity for India. Investors should position for a rotation into Indian large-cap equities and key index constituents as capital shifts away from Emerging Markets.

The global financial stage is set for a seismic shift as South Korea inches closer to MSCI Developed Market status. This reclassification will force a monumental reallocation of passive fund capital, presenting a golden opportunity for Indian equities. Our analysis reveals how India could become the primary beneficiary, attracting substantial inflows.

South Korea's MSCI Upgrade: A Tsunami of Capital Flowing Towards India?

The global investment landscape is abuzz with the prospect of South Korea shedding its Emerging Market (EM) classification for Developed Market status within the influential MSCI indices. This potential reclassification, while a landmark event for Seoul, carries profound implications for capital allocation across the globe, and most critically, for the Indian stock market. For investors navigating the complexities of global asset flows, understanding this impending shift is paramount. WelthWest Research Desk, through meticulous data analysis, presents a definitive guide to this pivotal moment, exploring the magnitude of capital movements, identifying the key beneficiaries and casualties, and outlining a strategic playbook for the discerning investor.

Why Does South Korea's MSCI Status Matter So Profoundly NOW?

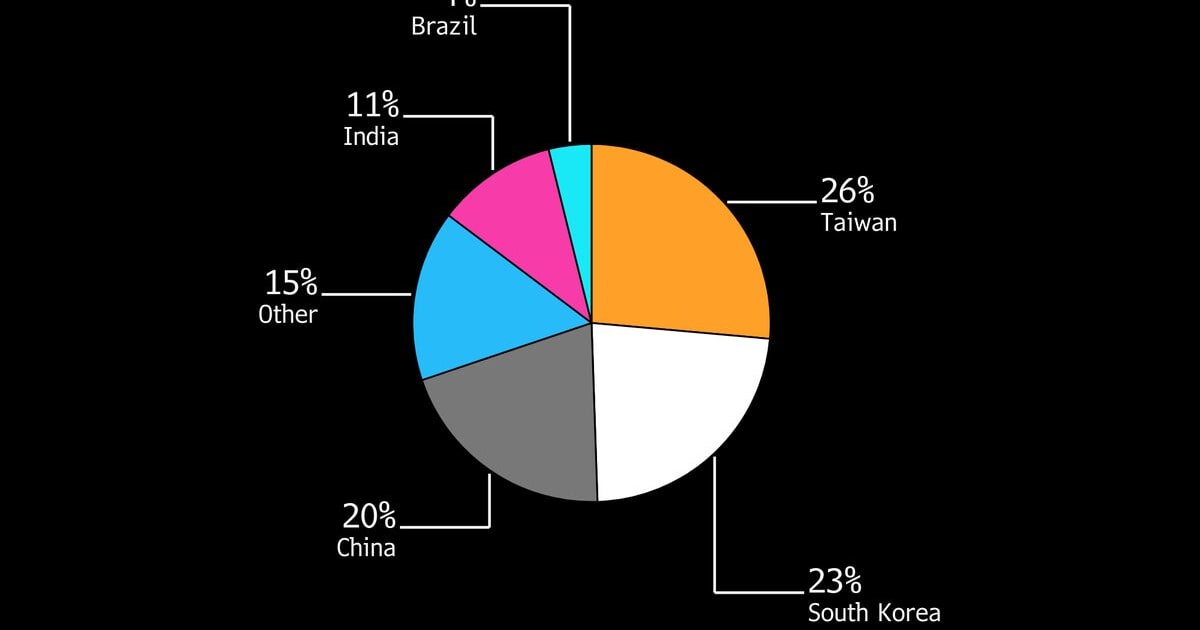

The MSCI index reclassification process is not merely an academic exercise; it is a powerful driver of global investment flows. When a market is upgraded or downgraded, it triggers automatic adjustments in hundreds of billions of dollars worth of passive investment funds, including Exchange Traded Funds (ETFs) and index-tracking mutual funds. These funds are designed to mirror the composition of specific indices, meaning they must buy or sell securities in proportion to their weight within the index. South Korea's current weight in the MSCI Emerging Markets Index is substantial, estimated to be around 12-14%, representing a significant chunk of the EM universe. A move to Developed Market status would necessitate the complete removal of South Korean equities from the EM index. This isn't a gradual process; it's a decisive pivot that forces global asset managers to rebalance their portfolios. The urgency is amplified because such reclassifications are often anticipated, allowing sophisticated investors to position themselves ahead of the official announcement, but the actual index inclusion or exclusion dates dictate the mandatory rebalancing. The primary driver for South Korea's consideration is its advanced economy, robust corporate governance standards, and open capital markets, criteria that have been progressively met over recent years.

The Deep Market Impact: India as the Primary Beneficiary of EM Capital Rotation

The exit of South Korean stocks from the MSCI EM Index will create a void that needs to be filled by other constituents, and India is exceptionally well-positioned to absorb this capital. As the second-largest constituent after China, India's relative weight within the EM index will naturally increase. More importantly, the capital exiting EM funds that were mandated to hold Korean stocks will need to be redeployed. Given India's status as a rapidly growing economy with a large and liquid equity market, it becomes the most logical and attractive destination for this displaced capital. We anticipate a significant inflow into Indian large-cap equities and companies that form the backbone of the MSCI India Index. Historically, similar reclassifications have demonstrated this effect. For instance, when Taiwan and South Korea were initially considered for Developed Market status in previous cycles, it led to noticeable shifts in EM flows, with markets like India seeing increased investor interest as a more stable and growth-oriented alternative within the EM space.

The magnitude of this potential reallocation is staggering. If passive funds tracking the MSCI EM Index hold upwards of $2 trillion, even a 10% allocation to South Korea translates to $200 billion that would need to be reallocated. While not all of this will flow directly into India, a substantial portion is expected to. This influx of foreign institutional capital can significantly boost market liquidity, support valuations, and drive stock prices higher. For India, this represents an opportunity to solidify its position as the de facto anchor of the MSCI EM index, attracting not just passive flows but also encouraging active fund managers to increase their allocations to capture the growth story.

How will the MSCI reclassification impact Indian sector performance?

The impact will be broadly positive across the Indian equity market, but certain sectors and their heavyweight constituents are poised to benefit disproportionately. Primarily, large-cap companies that are already significant components of the MSCI India Index will see increased buying pressure. These include sectors like Banking, Information Technology, and Reliance Industries, which dominate the index's composition. The banking sector, in particular, is a linchpin of the Indian economy and a favored destination for foreign capital due to its growth prospects and improving asset quality. Similarly, the IT sector, known for its global competitiveness, will benefit from increased liquidity and investor confidence in Indian equities as a whole. The broader impact will also be felt by mid-cap and small-cap stocks as overall investor sentiment towards India improves, leading to a 'halo effect' and potential spillover of capital into these segments.

Stock-by-Stock Impact Analysis: Key Indian Equities Set for a Boost

The impending MSCI reclassification of South Korea presents a clear opportunity for select Indian large-cap stocks. These companies, due to their significant weightage in the MSCI India Index and their status as bellwethers of the Indian economy, are prime candidates to receive substantial inflows as global capital rebalances.

- Reliance Industries (RELIANCE): As the largest company by market capitalization in India and a key constituent of the MSCI India Index, Reliance Industries is almost certainly to be a major beneficiary. Any increase in foreign institutional investment (FII) into India will naturally find its way into this behemoth. Its diversified business model, spanning petrochemicals, retail, telecom, and new energy, makes it a comprehensive play on India's growth story. An influx of capital can further support its ambitious expansion plans and potentially lead to a re-rating of its stock.

- HDFC Bank (HDFCBANK): The banking sector is a critical component of any emerging market's financial infrastructure, and HDFC Bank, as one of India's largest private sector lenders, is at the forefront. Its robust balance sheet, consistent profitability, and strong market share make it an attractive target for foreign investors seeking exposure to India's financial services growth. Increased FII inflows will directly translate into higher demand for HDFC Bank shares, potentially compressing its already competitive P/E ratio further.

- ICICI Bank (ICICIBANK): Similar to HDFC Bank, ICICI Bank's strong financial performance, digital transformation initiatives, and expanding customer base position it as a key beneficiary. As foreign investors look to diversify their EM exposure within India, ICICI Bank’s solid fundamentals will attract significant attention. The banking sector, in aggregate, is expected to see a substantial boost in foreign ownership.

- Infosys (INFY): The Indian IT sector is a global powerhouse, and Infosys, a leader in digital transformation and cloud services, is a prime example. As global demand for IT services remains robust, increased foreign investment in India will likely flow into its most established and reputable IT companies. Infosys's strong order book and consistent revenue growth (currently projected to be around 7-9% for FY25) make it a safe haven and growth stock within the EM context.

- Tata Consultancy Services (TCS): As the largest IT services company in India, TCS is another significant beneficiary. Its deep client relationships, expansive service offerings, and consistent execution will attract foreign capital seeking exposure to India's thriving technology sector. With a market cap exceeding $150 billion, even a marginal increase in FII allocation can lead to substantial price appreciation.

These large-cap stocks represent the core of the Indian equity market and will likely be the primary conduits for the capital rotation. Their substantial market capitalization ensures they can absorb significant inflows without undue price distortion, making them preferred destinations for index-aware funds and institutional investors.

Expert Perspectives: Bulls vs. Bears on the MSCI Shift

The debate surrounding South Korea's MSCI upgrade and its implications for India is spirited, with clear divergences between bullish and bearish outlooks.

Bullish Argument: "This is a textbook case of capital rotation driven by index rebalancing. India, with its superior growth trajectory, demographic dividend, and improving economic fundamentals, is the natural and most attractive destination for the trillions exiting EM funds due to Korea's upgrade. We anticipate a sustained period of strong FII inflows, boosting Indian valuations and creating significant alpha opportunities, particularly in large-cap growth stocks and key index constituents." - Senior Market Strategist, WelthWest Research Desk.

Bulls emphasize that the sheer size of the capital pool that needs rebalancing is unprecedented. They point to India's growing weight in global indices and its increasing prominence as a manufacturing and consumption hub as compelling reasons for sustained foreign investment. Furthermore, they highlight that the current geopolitical environment makes India an even more attractive diversification play compared to other EM peers.

Bearish Counterpoint: "While the potential for inflows is real, the market often prices in such events well in advance. The actual impact might be less dramatic than anticipated, and the process is inherently slow and subject to stringent MSCI criteria. Investors must also consider the global macroeconomic headwinds, such as persistent inflation and higher interest rates in developed economies, which could dampen overall investment appetite for riskier EM assets, irrespective of index reclassifications. Moreover, if South Korea fails to meet the final criteria, the expected capital flight might not materialize as swiftly, delaying any benefits for India." - Chief Economist, Independent Research Group.

Bears caution against over-optimism, highlighting that the MSCI upgrade process is not guaranteed and can be lengthy. They also point to potential global economic slowdowns and the possibility of other EM countries gaining prominence, diverting capital away from India. Concerns about valuation multiples in India, which are already at a premium compared to historical averages, are also cited as a reason for caution.

Actionable Investor Playbook: Navigating the MSCI Reclassification Opportunity

For investors looking to capitalize on this significant market shift, a strategic approach is essential. The primary objective is to position for increased foreign capital inflows into India, particularly into its most liquid and influential equities.

- Buy: Focus on large-cap Indian equities that are key constituents of the MSCI India Index. Specifically, consider increasing exposure to the banking and IT sectors. Stocks like RELIANCE, HDFCBANK, ICICIBANK, INFY, and TCS should be core holdings. Look for companies with strong fundamentals, consistent revenue growth, and healthy balance sheets.

- Consider Sector-Specific ETFs: For diversified exposure, consider India-focused ETFs that track the Nifty 50 or broader market indices, ensuring they have significant weightage in the aforementioned sectors and companies. Be mindful of ETFs with substantial Korean exposure, which might experience outflows.

- Entry Points: While the long-term trend is likely bullish, short-term volatility is always possible. Investors might consider accumulating positions on any dips or pullbacks in the market, rather than chasing immediate rallies. A phased entry approach over the next 3-6 months is advisable.

- Time Horizon: The full impact of such a reclassification unfolds over several quarters, not days or weeks. Investors should adopt a medium-term to long-term investment horizon (1-3 years) to fully realize the benefits of sustained foreign capital inflows.

- Watch: Monitor the official announcements from MSCI regarding South Korea's inclusion in the Developed Markets index. Also, keep a close eye on the net FII inflows into India.

Risk Matrix: Navigating the Uncertainties of MSCI Reclassification

While the opportunity is significant, potential risks must be carefully considered. The MSCI reclassification process is inherently complex and subject to external factors.

- Risk of Delayed or Denied Upgrade (Probability: Medium): MSCI's criteria are stringent and subject to review. South Korea might not meet all requirements, or the process could be significantly delayed, postponing the expected capital rotation into India. This would dampen the immediate impact.

- Global Macroeconomic Headwinds (Probability: High): Persistent global inflation, rising interest rates in developed economies, and potential recessions could lead to a general risk-off sentiment, reducing overall foreign investment appetite for emerging markets, including India. This could offset the positive impact of the reclassification.

- Valuation Concerns in India (Probability: Medium): Indian equities are trading at a premium compared to historical averages and many global peers. A significant inflow of capital could further inflate valuations, making the market more vulnerable to corrections if growth falters or global sentiment shifts abruptly.

- Geopolitical Instability (Probability: Low to Medium): Unexpected geopolitical events or regional conflicts could create market volatility and deter foreign investment in emerging markets, overriding the positive impact of the MSCI reclassification.

What to Watch Next: Catalysts and Data to Monitor

The narrative surrounding South Korea's MSCI status and its impact on India will be driven by several key catalysts and data releases in the coming months:

- MSCI Consultation Outcomes: Closely follow MSCI's periodic consultations and announcements regarding the potential reclassification of South Korea. These provide crucial signals about the timeline and likelihood of the event.

- Foreign Institutional Investor (FII) Flows: Daily and weekly data on FII inflows into the Indian equity market will be a direct indicator of how capital is reacting to the evolving situation. Significant and sustained inflows will validate the bullish thesis.

- India's Economic Data: Key economic indicators from India, such as GDP growth rates, inflation figures, and manufacturing/services PMI, will be crucial in maintaining India's attractiveness as an investment destination.

- South Korean Market Performance: Monitor the performance of South Korean equities. Any significant outflows or underperformance could signal that the market is anticipating the reclassification and its consequences.

- Global Central Bank Policies: Decisions by major central banks (e.g., the US Federal Reserve, European Central Bank) on interest rates and quantitative easing will significantly influence global liquidity and risk appetite, impacting FII flows into emerging markets.

The potential MSCI upgrade for South Korea is more than just an index adjustment; it represents a significant tectonic shift in global capital allocation. For India, it presents a golden opportunity to attract substantial foreign investment, bolstering its equity markets and potentially driving a new phase of growth. By understanding the dynamics, identifying the key beneficiaries, and managing the associated risks, investors can strategically position themselves to benefit from this pivotal moment in emerging market investing.

Disclaimer: This content is generated by WelthWest Research Desk based on publicly available reports and is for informational purposes only. It does not constitute financial advice, investment recommendations, or an offer to buy or sell securities. Always consult a qualified financial advisor before making investment decisions.