Key Takeaway

The potential withdrawal of the Yinson privatization bid by Stonepeak and the Lim family signals a widening valuation gap and tightening liquidity in the global energy infrastructure sector, acting as a cautionary signal for Indian offshore service providers.

The collapse of the multi-billion dollar privatization bid for Yinson Holdings Bhd by Stonepeak Partners and the founding Lim family highlights a critical shift in how private equity views capital-intensive energy assets. While primarily a Malaysian event, the implications for Indian energy giants and offshore service providers are profound, suggesting a re-rating of exit valuations and a more disciplined approach to infrastructure CAPEX. Investors must now navigate a landscape where high interest rates and ESG pressures are forcing a fundamental rethink of asset pricing in the deepwater and FPSO sectors.

The Tectonic Shift in Energy Infrastructure: Why the Yinson Stalemate Matters

The global energy infrastructure landscape is witnessing a significant tremor. News that Stonepeak Partners and the Lim family are considering withdrawing their bid to privatize Yinson Holdings Bhd—a global leader in Floating Production Storage and Offloading (FPSO) units—is not merely a localized Malaysian corporate event. It is a symptomatic failure that highlights a deepening disconnect between public market valuations and private equity expectations in the energy sector.

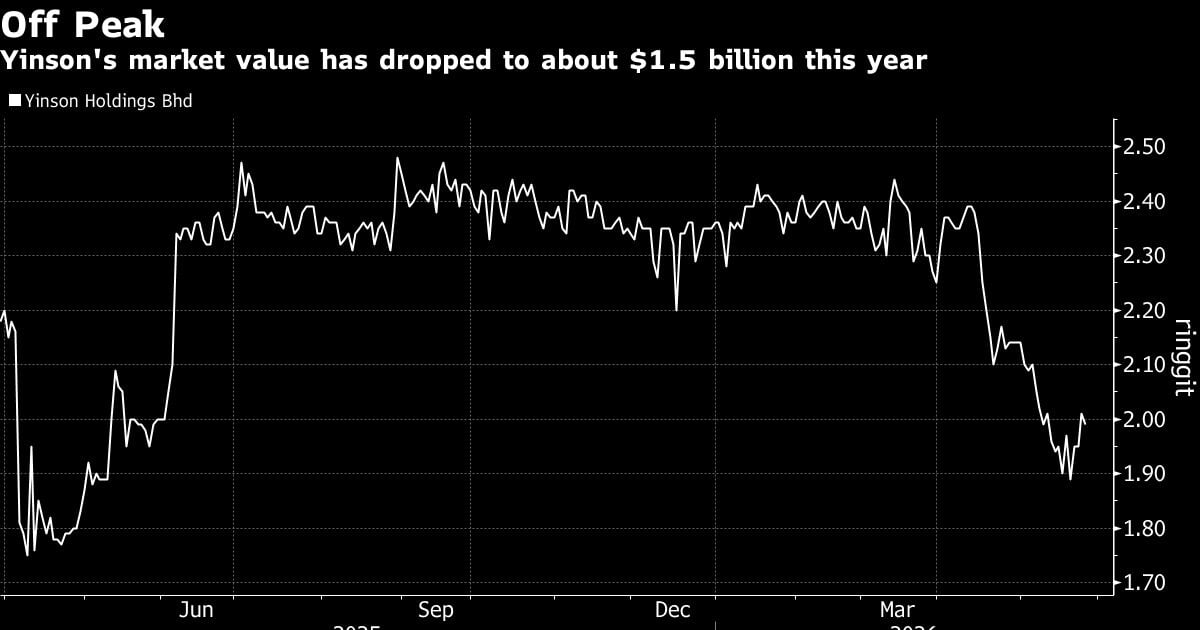

For the uninitiated, Yinson is a titan in the offshore services space, commanding a market capitalization of approximately 7.5 billion MYR ($1.6 billion). The privatization bid was seen as a move to unlock value away from the scrutiny of public markets, allowing the company to aggressively expand its FPSO fleet and renewable energy portfolio. However, the potential withdrawal of this bid suggests that the Weighted Average Cost of Capital (WACC) for such massive, debt-heavy infrastructure projects is no longer aligning with projected Internal Rates of Return (IRR).

In the world of high-finance, when a firm like Stonepeak—which manages over $70 billion in assets—hesitates on a deal of this magnitude, it sends a clear signal: the 'easy money' era for energy infrastructure is over. This development serves as a critical bellwether for Indian markets, particularly for companies involved in deepwater exploration and offshore logistics, where capital intensity is high and the margin for error is thinning.

The Anatomy of the Yinson-Stonepeak Friction: A Valuation Gap Widens

Why would a deal of this strategic importance falter now? The primary culprit is the valuation gap. Public markets have been conservative in pricing energy service stocks, often applying a 'green discount' to companies with legacy oil and gas assets. Private equity, conversely, has historically been willing to pay a premium for steady, long-term cash flows from FPSO contracts. However, with global interest rates remaining 'higher for longer,' the cost of financing these multi-billion dollar buyouts has surged.

Yinson’s business model relies on massive upfront CAPEX to build FPSOs, which are then leased to oil majors like Petrobras or Eni under long-term contracts. In a 2% interest rate environment, this is a goldmine. In a 5% environment, the debt serviceability eats into the equity IRR, making the privatization price hard to justify. This is a bearish signal for the sector, indicating that even the most stable infrastructure assets are facing valuation headwinds.

How will the Yinson deal collapse affect Indian offshore stocks?

While Yinson is a Malaysian entity, the energy service market is global. Indian companies like ONGC and Reliance Industries compete for the same offshore vessels, technical expertise, and capital pools. If global PE sentiment sours on offshore infrastructure, the ripple effects will be felt on Dalal Street through three primary channels:

- Benchmarking Multiples: Indian offshore service providers often use global peers like Yinson or SBM Offshore as valuation benchmarks. A failed privatization suggests that these benchmarks may be inflated, leading to a potential de-rating of Indian mid-cap energy stocks.

- Cost of Equipment: A slowdown in Yinson's expansion could lead to a temporary glut in FPSO components, potentially benefiting Indian explorers like ONGC in terms of lower charter rates. However, it also signals a lack of confidence in long-term offshore production growth.

- Exit Strategies: Indian infrastructure funds looking to exit their energy holdings via PE buyouts may find the market much colder, forcing them to hold assets longer or accept lower valuations.

Deep Dive: Impact on the Indian Energy Ecosystem

Historically, when global energy infrastructure deals fail due to financing hurdles, the Indian Nifty Energy Index tends to exhibit volatility with a lag of 2-4 weeks. During the 2014-2015 offshore downturn, a similar cooling of PE interest preceded a 15% correction in Indian offshore service stocks. Today, the situation is more nuanced, but the risk of a 'valuation reality check' is high.

Stock-by-Stock Breakdown: Indian Tickers in the Crosshairs

To understand the practical impact, we must look at specific NSE/BSE listed entities that operate in the shadow of global energy infrastructure trends.

1. Oil and Natural Gas Corporation (ONGC) | NSE: ONGC

The Connection: ONGC is currently aggressively pursuing deepwater projects in the KG Basin. These projects require the very FPSO technology that Yinson specializes in. If Yinson faces internal restructuring or financing constraints, the availability and pricing of FPSO charters for ONGC could become volatile. Furthermore, ONGC's own valuation as a 'value stock' is tied to the global perception of offshore asset longevity. A bearish sentiment in PE for these assets limits the upside for ONGC’s P/E multiple, which currently hovers around 6.5x.

2. Great Eastern Shipping Co Ltd (GESCO) | NSE: GESHIP

The Connection: GESCO’s offshore division (Greatship) is a direct beneficiary of a buoyant offshore market. With a fleet of Jack-up rigs and OSVs, GESCO relies on the CAPEX cycles of global giants. If Stonepeak is pulling back, it suggests a broader caution in the offshore CAPEX cycle. GESCO, trading at a P/B ratio of 1.4x, could see its offshore segment’s valuation come under pressure if the market perceives a peak in the current cycle.

3. Larsen & Toubro (L&T) | NSE: LT

The Connection: L&T’s Hydrocarbon segment is a powerhouse in offshore EPC (Engineering, Procurement, and Construction). They build the platforms and modules that integrate with FPSOs. A slowdown in the privatization and subsequent aggressive expansion of firms like Yinson indicates a potential slowing of the global order book. While L&T has a robust domestic pipeline, its international margins are sensitive to the global PE appetite for energy infra.

4. Mazagon Dock Shipbuilders | NSE: MAZDOCK

The Connection: While primarily a defense player, Mazagon Dock is the premier Indian yard for offshore platform repairs and specialized vessel construction. A bearish shift in global offshore sentiment could lead to a 'wait and watch' approach from domestic private players who utilize these yards, potentially impacting the non-defense revenue stream of MAZDOCK.

5. Reliance Industries Ltd (RIL) | NSE: RELIANCE

The Connection: Reliance’s deepwater gas assets in the MJ and R-Cluster fields are world-class. However, RIL is also a massive investor in the global energy transition. The Yinson deal’s failure—partly due to the difficulty of valuing 'transitioning' energy firms—mirrors the challenges RIL faces in spinning off or valuing its O2C (Oil-to-Chemicals) vs. New Energy businesses. It highlights the difficulty of getting 'fair value' for integrated energy assets in the current market.

Expert Perspective: The Bull vs. Bear Argument

"The Yinson situation is a classic case of 'Cost of Capital' vs. 'Asset Quality.' The assets are great, the contracts are solid, but the math doesn't work at a 9% discount rate when it worked at 5%. Indian investors should view this as a signal to prioritize companies with zero debt and high internal cash generation." — Senior Analyst, WelthWest Research

The Bear Case: Bears argue that this is the 'canary in the coal mine.' If a firm as established as Yinson cannot secure a privatization premium, it means the terminal value of offshore oil assets is being aggressively discounted due to ESG mandates. They foresee a sharp sell-off in energy service providers as liquidity dries up.

The Bull Case: Contrarians argue that this deal failure is actually bullish for existing players. If privatization fails and capital becomes scarce, it prevents oversupply in the market. This 'capital discipline' ensures that charter rates for FPSOs and rigs stay high, benefiting the incumbents who already have their fleets in place.

Actionable Investor Playbook: Navigating the Energy Infra Chill

Based on this analysis, investors should consider the following tactical moves:

- Short-Term (0-3 Months): Avoid adding new positions in high-beta offshore service stocks. Expect volatility in ONGC and GESHIP as the market digests global PE sentiment.

- Medium-Term (6-12 Months): Look for entry points in L&T. Their diversified order book provides a hedge against a purely energy-driven slowdown. If the stock corrects 5-8% on global energy news, it becomes an attractive 'buy on dips' candidate.

- The 'Safety' Play: Shift focus toward energy companies with high dividend yields. If growth multiples are being compressed, the 'bird in hand' (dividends) becomes more valuable. ONGC’s dividend yield (approx. 5%) provides a floor to its stock price.

- Watch the Yield Curve: Any softening in US Treasury yields will be the primary catalyst for these deals to return to the table. Monitor the 10-year yield closely.

Risk Matrix: Assessing the Fallout

| Risk Factor | Probability | Impact on Indian Market |

|---|---|---|

| Contagion to Other PE Deals | High | Could stall similar infrastructure buyouts in India's renewable and road sectors. |

| Sharp Drop in Yinson Shares | Very High | Will lead to a sentimental sell-off in global energy service ETFs, affecting FII flows into Indian energy. |

| Oil Price Volatility | Medium | If Brent drops below $75, the rationale for high-cost offshore projects evaporates, compounding the deal failure. |

What to Watch Next: The Upcoming Catalysts

The story doesn't end with a withdrawn bid. Investors must keep an eye on these critical data points:

- Yinson’s Quarterly Earnings (Expected next month): Watch for management commentary on debt restructuring and CAPEX guidance.

- The Federal Reserve’s Next Move: Any hint of a rate cut in late 2024 could reignite the privatization talks as financing costs drop.

- Indian Ministry of Petroleum Announcements: Any new deepwater licensing rounds or changes in windfall tax will dictate how much domestic players care about global PE sentiment.

In conclusion, the Stonepeak-Yinson saga is a masterclass in the importance of capital discipline. For Indian investors, it is a reminder that in the world of heavy infrastructure, the 'deal' is only as good as the debt that finances it. Stay cautious, prioritize cash flow, and watch the global benchmarks.

Disclaimer: This content is generated by WelthWest Research Desk based on publicly available reports and is for informational purposes only. It does not constitute financial advice, investment recommendations, or an offer to buy or sell securities. Always consult a qualified financial advisor before making investment decisions.